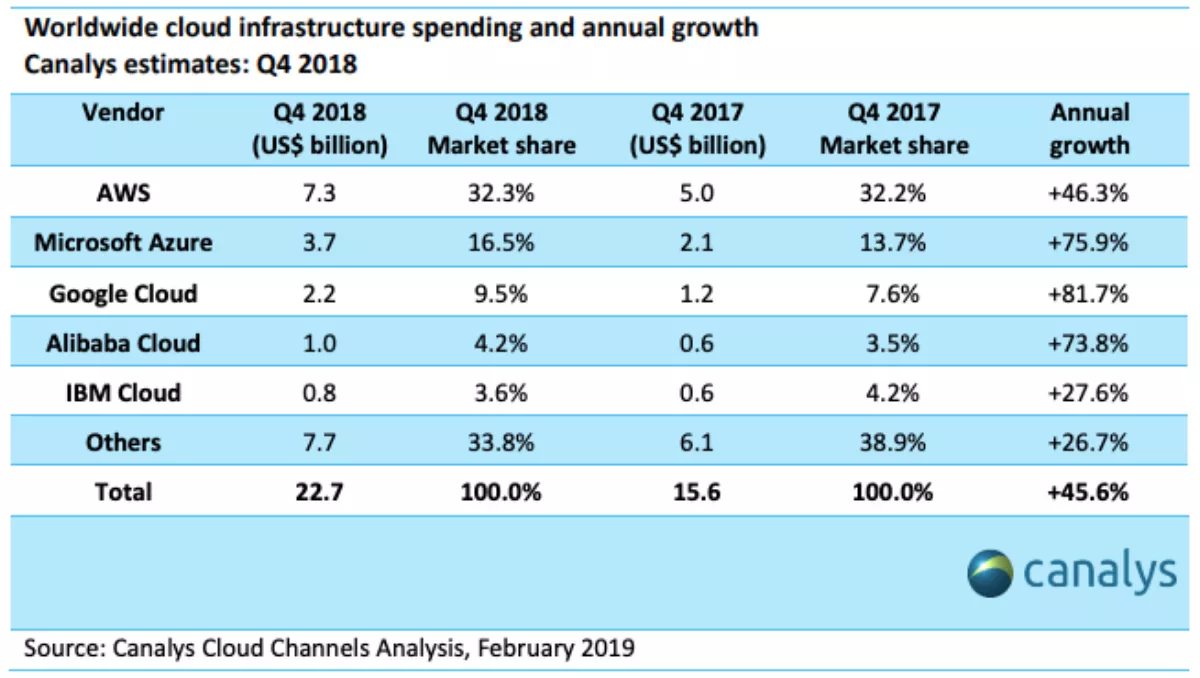

The worldwide cloud infrastructure market had another strong quarter in Q4 2018, as spending grew 46% to nearly US$23 billion.

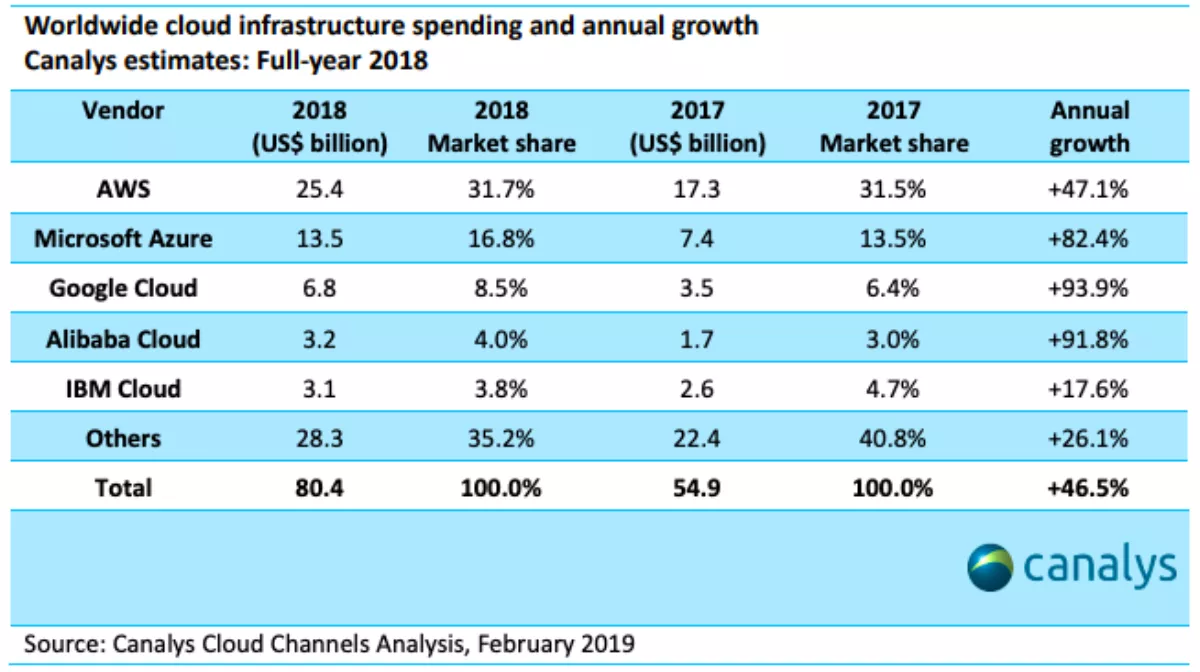

Total outlay on cloud infrastructure in 2018 exceeded US$80 billion, up from US$55 billion in 2017 according to Canalys data.

This makes it one of the most important sectors in the IT industry, not just by the rate of growth, but also its expanding size.

Amazon Web Services (AWS) remained the dominant cloud service provider in Q4 2018, its share of customer spend unchanged at 32%.

Microsoft Azure grew its share to 16% against 14% in the same period a year ago.

Google Cloud hit 9% for the first time, while Alibaba Cloud maintained its 4% share.

IBM, Salesforce, Oracle, NTT Communications, Tencent Cloud and OVH rounded out the top 10 cloud service providers.

"Cloud infrastructure services provide the core components needed to support businesses' digital transformation initiatives around building new customer experiences, deploying IoT to transform processes, using big data and analytics for better insights, and embedding machine learning and AI for automation," says Canalys principal analyst Matthew Ball.

"Market dynamics have changed over the last 12 months, with more businesses opting for multi-cloud and hybrid-IT environments to use the strengths of different cloud service providers and deployment models dependent on application and data requirements, compliance, cost and performance.

The role of channel partners in cloud services is growing in importance as a direct result of these trends, in particular, understanding customer requirements, recommending services, deployment and integration, as well as simplifying the billing and management of multiple cloud services.

"Cloud service providers are placing greater emphasis on building channel programs to support the growing network of partners beyond the largest systems integrators, especially as they extend to mid-market and SMB customers," says Canalys chief analyst Alastair Edwards.

"Canalys expects the share of cloud business handled by or with channel partners to increase in 2019. Cloud service providers must, therefore, find ways to improve their own differentiation to partners and raise the maturity of their channel models.

Canalys expects a greater focus on rewarding partners with specialist expertise around specific cloud deployments, such as SAP HANA, analytics or security; on partners developing unique services on top of cloud; and on those driving customer adoption of cloud services.

"Cloud service providers need to build trust with channel partners and not implement initiatives or change terms and conditions that drive more direct sales," adds Edwards.

"Microsoft is the current dominant force in the channel for cloud services, through the continued expansion of its Cloud Solution Provider (CSP) programme. But as it offers more direct purchasing options to Azure customers through its new Microsoft Customer Agreement, its partner strategy faces increased scrutiny. This creates an opportunity for rivals to exploit growing uncertainty among Microsoft's partners.