IDC: No recovery in sight for semiconductor market

Tue, 5th May 2020

Ahead of the COVID-19 virus, worldwide semiconductor revenue declined 12.2% in 2019 to $418 billion, according to the latest update of the IDC Semiconductor Applications Forecaster (SAF).

The global economy in 2019 grew at its slowest pace since the global financial crisis in 2008, and US-China trade disputes grounded semiconductor sentiment and demand.

Higher levels of inventory in specific areas like mobile phones and cloud infrastructure brought pricing pressure and negatively impacted semiconductor sales.

Driving the downturn were declines of 37.3% and 27.7% in the DRAM and NAND markets respectively, after more than two years of strong growth.

While most companies witnessed revenue declines in 2019 a few outperformed the market. Intel regained its leadership in the market becoming once again the largest company in terms of revenues – due to a more diversified business seeing solid returns and better than expected PC demand from the Windows refresh in enterprise.

MediaTek and AMD also grew revenues significantly last year as both companies began to see strong traction in their respective core businesses and gained market share.

Sony achieved the highest growth among the largest semiconductor companies with its image sensor business taking advantage of the adoption and growth in the number of cameras on flagship smartphones.

Instead of an anticipated bottom and gradual recovery in 2020, the emergence of COVID-19 will drive another contraction in the overall semiconductor market.

"The strength in demand in March and early April have made computing, connectivity, and memory products more resilient. However, the global shelter in place orders and ongoing shift in buying behaviour toward essential goods and services will negatively impact consumer and business spending in the second quarter and second half of the year," says IDC semiconductors programme vice president Mario Morales.

"The nature of the recovery will highly depend upon how quickly government stimulus plans to stabilise the global macroeconomy and consumer confidence. As we reopen across the globe, including our borders, how long will it take us to get back to normal and start rebuilding our lives from the shock of the pandemic?"

Based on the latest information available, IDC expects the overall semiconductor market to decline by 4.2% as the global economy fights to recover from this unprecedented crisis in 2020.

Excluding the DRAM and flash markets, semiconductors are expected to decline by 7.2%. The demand for semiconductors will be very uneven across the different industry markets.

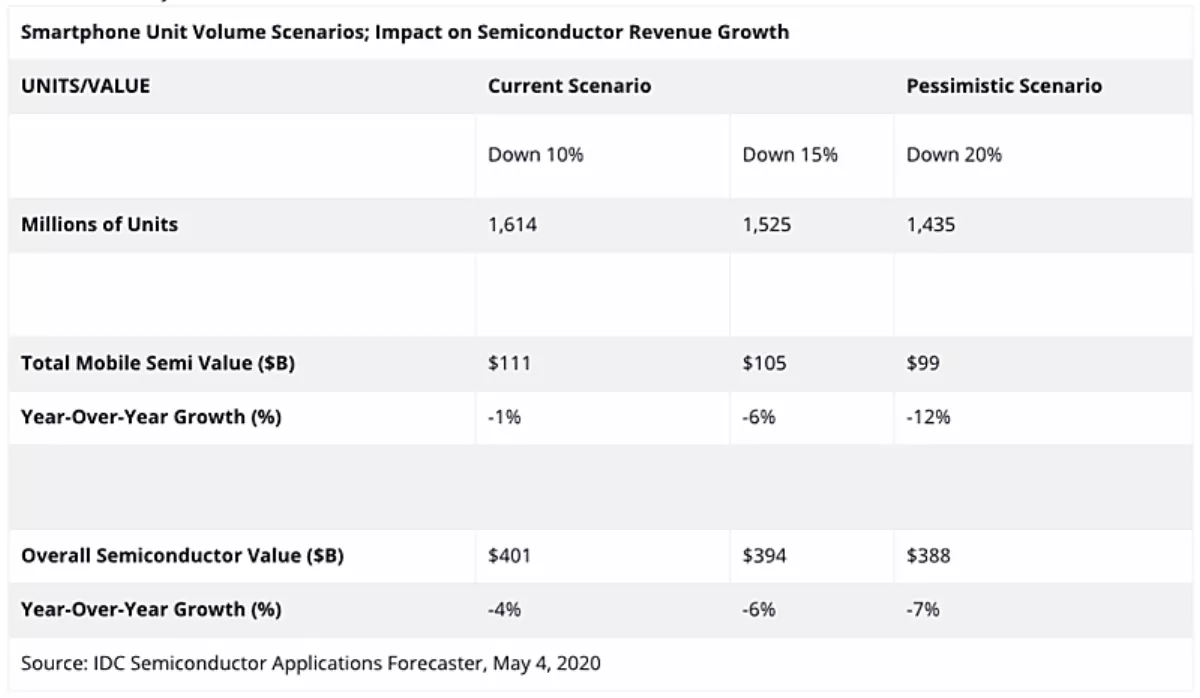

Smartphones will continue to be the largest demand driver and will remain weak overall given the concentration in volumes being 4G.

A large Chinese OEM will need to work down inventories after stuffing the channel over the past couple of quarters.

This will drive the rest of the OEMs in China to concentrate on launching 5G devices to leverage potential subsidies by carriers later this year.

IDC expects 5G volumes will grow this year despite the demand uncertainty, driving strong semiconductor content as OEMs position 5G in lower tiers to broaden the reach. There are 5G phones that have started selling for under $300 in China.

Every per cent drop in smartphone unit volume expectations will have a couple of percentage points of impact on overall semiconductor revenues for the year.

The impact of COVID-19 and the subsequent shelter in place orders and shutdowns have had an uneven impact on the semiconductor markets.

"While some consumer areas will initially benefit from the adjustment to new situations, we expect reductions in consumer spending lasting deep into 2021 – given never before seen unemployment levels," adds IDC semiconductors and enabling technologies research director Michael Palma.

"We also expect reduced spending on industry-specific verticals and digital transformation efforts among a wide range of enterprises, especially those dependent on consumer spending, such as the hospitality, retailing, and manufacturing sectors."

For the year, IDC expects the consumer segment to see non-memory consumer semiconductor revenues decline 11.5% year over year in 2020.

The automotive and industrial semiconductor markets – which in the past were projected to outperform the other segments – have been particularly hit hard by the COVID-19 mandates.

Automobile sales including light commercial vehicles in 2019 declined 5.6% to 81.4 million vehicles, resulting in a decline in automotive semiconductor growth by 2.7% to $38.4 billion.

Industrial semiconductors also experienced a downturn in 2019, down 6.6% year over year to $37.8 billion.

Previously forecast to recover slightly in 2020, IDC's new forecast projects a decline of 11.4% in 2020.

As companies reduce manufacturing in response to the global economic slowdown and changes in consumer spending, the impact on the industrial market will negatively affect industrial semiconductor revenue through 2021.