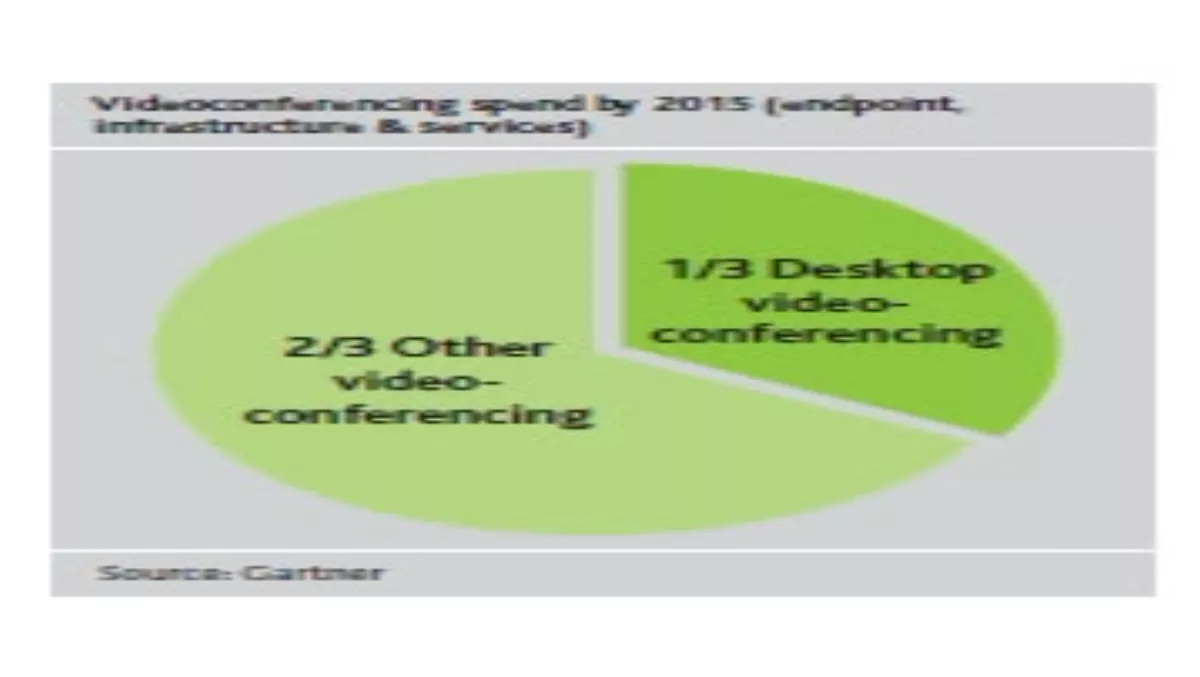

The market is also a lot less standardised in terms of the types of devices out there these days. When it comes to monitors there is the choice between standard aspect and widescreen, LDC or plasma, and touchscreen technology is also taking off. Monitors are not simply sold as an accessory to the PC anymore and the number of monitor-only sales opportunities is increasing. Frost & Sullivan's Research Director, Australia and New Zealand, ICT, Audrey William says “the display market continues to see good growth of about 20% - the decline in price points for both the plasma and LCD players will drive demand further in the market.”While the decision to choose widescreen versus standard aspect monitors, or to go with LCD over plasma will be dictated by the requirements of the monitor's new environment, there is a greater emphasis on the software that drives it. Frost & Sullivan's William says the major trends in digital media today are touchscreen technology, interactivity between digital signage display systems and mobile phones, and facial recognition technology for digital signage that can help identify a buyer's attitude towards the product through emotion detection capability.Pointing it outDigital signage has gained momentum over the past two years and is no longer simply a sub-class of monitors, but includes 3D screens, touchscreen technology, biometrics and facial recognition technology. Gartner's Hype cycle for retail technologies, 2009, lists its market penetration as only 1% to 5% of the target audience; the optimistic amongst us will see this as a big opportunity. While it's widely accepted that 70% of purchase decisions are made when the customer is actually shopping in a physical store, Gartner listed “effectiveness of content” as a challenge and the greatest barrier to success. If you do choose to deploy a digital signage solution, seek expertise to help design the content and its refresh strategy. A more recent Gartner report, In-store digital marketing must evolve to influence consumers, showed the results of a survey of types of in-store marketing.Interactive in-store marketing techniques such as web-enabled dressing rooms have more impact than other mediums and tend to infl uence the youngest customers the most.Frost & Sullivan's William sees the opportunities in the digital signage display and software market as “immense” since the market is still in its early stages of growth in Australia. A digital signage solution sale includes media players, content and server management software, media player software, display mounts, installation costs, content development and maintenance, service, technical support and updates, as well as the monitors themselves.On screenMonitors are also becoming increasingly popular, thanks to the explosion of video and videoconferencing. The Gartner predicts 2010: video, cloud and UC services loom large in enterprise communication report suggests that by 2015, over 200 million workers globally will run corporate-supplied videoconferencing from their desktops, which means there will likely be a need for monitor upgrades. Desktop videoconferencing will grow from 13.9% of spending on videoconferencing endpoints, infrastructure and services, to one-third of the corporate spending on videoconferencing by 2015. As the younger, more video-primed 'Generation V' prepares to enter the workforce, corporate strategies must be realigned and budget made available for the video-based tasks.The third dimension3D TV is all the rage with retail vendors at present and, while adoption will most likely start in the home, it is a good idea to keep an eye on the technology for possible sales opportunities in the future. A Gartner report entitled Emerging technology analysis: It will take more than Avatar to drive mass adoption of 3D LCDs, advises vendors to “monitor, but not follow the hype around 3D TV”. Availability of content for TV and PC, plus new user experiences such as playback of images from 3D cameras and 3D video via the internet, or 2D-to-3D conversion, will most likely drive the technology's adoption. However, 3D has yet to prove that it offers sustainable longterm growth, says the research firm.Projecting an imageThings are also evolving in the projector market. When projector prices fell some time ago, it could have heralded problems, but vendors combated the potential slump by focusing on specialised models, such as the ultra-portable market, wireless projectors and short-throw projectors. The type of projection device sold will vary depending on its proposed use: a road-warrior will likely want a portable device that weighs less than two kilos with an instantoff function and colour-correction options for projecting images onto a coloured wall. Alternatively a fully equipped boardroom may allow for a variety of device inputs, all pre-wired at the time of building or installation.As projector technology improves, the devices seem to be less dependent on ambient light conditions and screen choices. That being said, the right screen can produce far better image results. Added to this, there is the potential for better margin when selling larger size, professional grade or speciality screens.

According to a recent electronics industry report by research company Pacifi c Media Associates, projectors using 3LCD technology comprised about 51% of the world's digital projector market in 2009. For mainstream projectors, themain competitor to 3LCD technology is singlechip DLP technology. Your choice of technology will likely depend on the content your client intends to screen. Of course, one of the biggest considerations when choosing a projector is the lamp. During the recession vendors noticed that more customers were replacing the lamp than had previously been the case, which opened up a new avenue of opportunity for resellers.Petite projectorsA 2009 Gartner report (Emerging technology analysis: pico projectors, PC technologies) also highlighted the emergence of 'pico' or very small projectors. The fi rst generation of these tiny projectors, so small they can be embedded in mobile phones for example, began to appear in 2009. User demand remains low at present and will take several years to become established, but they do represent a whole new way of selling projection devices. The small pico projector modules of 2009 had a volume of between 10 cc and 15 cc, and Gartner says we can expect future generations of the technology to be between 5 cc and 10 cc, “making integration into personal devices, such as handsets, more practical”.There are some rather exciting consequences of the pico projector, as they enable electronics manufacturers to move beyond the limitations of display panels. “Possibilities include developing 'human-machine' interfaces by integrating sensing and artifi cial intelligence technologies and new markets, such as interactive toys, pocket projectors or new applications, by combining pico projectors with wireless input/output devices like Bluetooth headphones or keyboards,” said the report. Pico projectors are likely to fi rst appear in hardware devices as premium features, but could eventually become an alternative to he conventional embedded display.The business implications are likely to be both exciting and compelling, such as instant presentations projected on a desktop to display information in a brief, face-to-face sales meeting, which makes this space one to watch. For more ideas on devices that could potentially house an embedded pico projector, see the accompanying table above.

A shining path

The digital media market is so much more than displays and projectors these days, and with this wealth of exciting, and let's face it, pretty sexy technology, there are plenty of sales opportunities. Now, when you are solving a client's visual display problem there are some really interesting and appealing options on offer.